Various categories of property transactions are undertaken in the South African property market, including in terms of undeveloped land, residential, commercial, industrial and agricultural land. Estate agents, being predominantly involved in selling, buying and renting properties on behalf of owners and purchasers, are generally seen as the first point of contact in a property transaction and therefore it is vital that potentially illicitly gained funds are identified at this stage.

Property provides a secure, liquid asset for money launderers to make use of in their schemes and allows them to clean their illicitly gained funds through the purchase of a stable asset by providing them with a potentially high yielding investment to provide ongoing benefits, for example by securing legitimate funds through monthly rental payments.

Various techniques are used by property-related money launderers such as the over or under value of property prices when compared to market-related pricing, cancelling property transactions prematurely, or paying rent in advance, and then requesting a refund, or purchasing properties using complex company or trust structures to conceal the identity of the launderer.

Estate agencies have filed an average of 6910 Cash Threshold Reports per year between April 2016 and March 2021. The prevalence of cash, particularly used in terms of the rental of business and office space, its inherent anonymity and difficulty in deciphering its source, is a considerable red flag for estate agencies accepting this mode of transfer. Practically speaking, cash may be paid into a Conveyancer’s or Attorney’s trust account, who may be seen as gatekeepers of access to accounts in the formal financial system at arm’s length from the Bank itself, and used as alternatives to legitimise illicitly gained cash.

Several risk factors should be considered by estate agents when dealing with their clients. Where considerable deposits are paid for the purchase of properties or high-value property is being purchased, more stringent measures should be implemented to ascertain the source of funds for the transaction and also whether the amount appears to be within the apparent standing or economic profile of the client and their stated income and that the transaction makes economic or business sense.

Estate agents should also bear in mind higher risk relationships with Domestic Prominent Influential Persons (DPIPs) or Foreign Prominent Public Officials (FPPOs) and incorporate this risk factor into their risk rating schemes. DPIPs and FPPOs are considered higher risk due to the status derived from their bureaucratic power and their ability to leverage departments for their resources. In addition, other risk factors include clients who are from countries that are regarded as being at higher risk for target by money launderers identified by the FATF as having AML/CFT weaknesses, countries subject to a travel ban or countries regarded as tax havens. (As of 29 December 2022, Domestic Prominent Influential Persons (DPIPs) and Foreign Prominent Public Officials (FPPOs) have been replaced with the acronyms Domestic Politically Exposed Persons (DPEPs) and Foreign Politically Exposed Persons (FPEPs). Read more here.)

In terms of terrorist financing risk, estate agencies that enter into business relationships with non-profit and non-governmental organisations should ensure that the related properties and funds used are within the overarching ambit of that organisations principles and purpose. Knowledge and utilisation of screening of clients against the United Nations Targeted Financial Sanctions Lists could mitigate these terrorist financing risks and better enable estate agents to make decisions regarding entering into transactions with sanctioned individuals or entities. The Report concludes that for the estate agency sector, the inherent money laundering risks are high and terrorist financing risks are low.

The Impact of the PPA on the FICAA

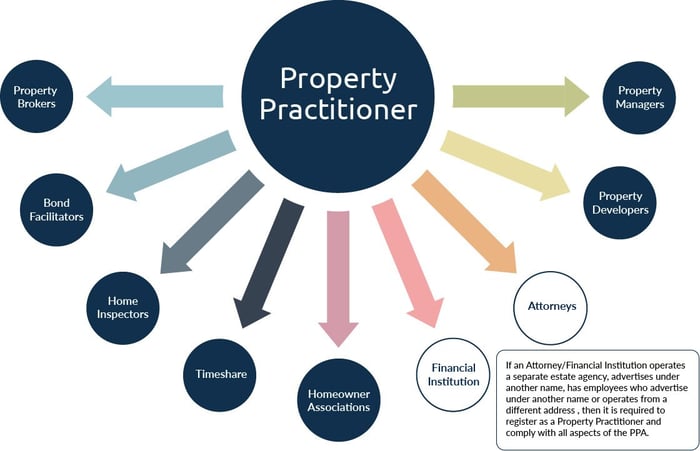

As mentioned previously , a Property Practitioner extends to not only estate agents but also property brokers, property developers and managers, bond facilitators and homeowner associations to name a few. In terms of Schedule 1 of the Financial Intelligence Centre Amendment Act (FICAA), only estate agents are listed as an Accountable Institution and therefore are mandated to comply with the full suite of FICAA obligations. The question to be asked therefore is will Schedule 1 Item 3 be amended to replace “estate agent” with “property practitioner”? As the Report mentions, the FIC has not yet consulted with the wider sector of property practitioners with respect to the above mentioned amendment to broaden the scope of Item 3.

However, Property Practitioners would be well advised to start thinking about how they can put processes and controls in place in their businesses to ensure their FICAA compliance as the amendment is not a situation of “if” it will happen but rather “when”.

Why not talk to our Compliance Services Team to see how we can help you be confident in your FICAA compliance with an independent audit of your files and processes, or prepare you to be ready for the pending Schedule Amendment that will make property practitioners fully accountable for FICA.